IRA Contributions with AGI Over $2 Million: What You Need to Know

Navigating the complexities of retirement savings can be daunting, especially when your income reaches higher levels. Many high-income earners find themselves asking: what are the rules for ira contribution if agi is over $2m? This comprehensive guide will delve into the limitations, alternative strategies, and essential considerations for individuals whose adjusted gross income (AGI) exceeds this threshold. We aim to provide clarity and actionable insights to help you optimize your retirement planning, even with significant income.

This article will cut through the jargon and provide a clear path forward, exploring contribution options, backdoor Roth strategies, and other advanced techniques. Our goal is to empower you with the knowledge to make informed decisions about your retirement future. You’ll gain a deep understanding of the current regulations, potential pitfalls, and how to maximize your retirement savings, no matter your income level.

Understanding IRA Contribution Limits and AGI

To fully grasp the implications of an AGI over $2 million on IRA contributions, it’s crucial to understand the fundamental rules governing Individual Retirement Accounts (IRAs). Traditional and Roth IRAs are powerful tools for retirement savings, but they come with specific contribution limits and income restrictions.

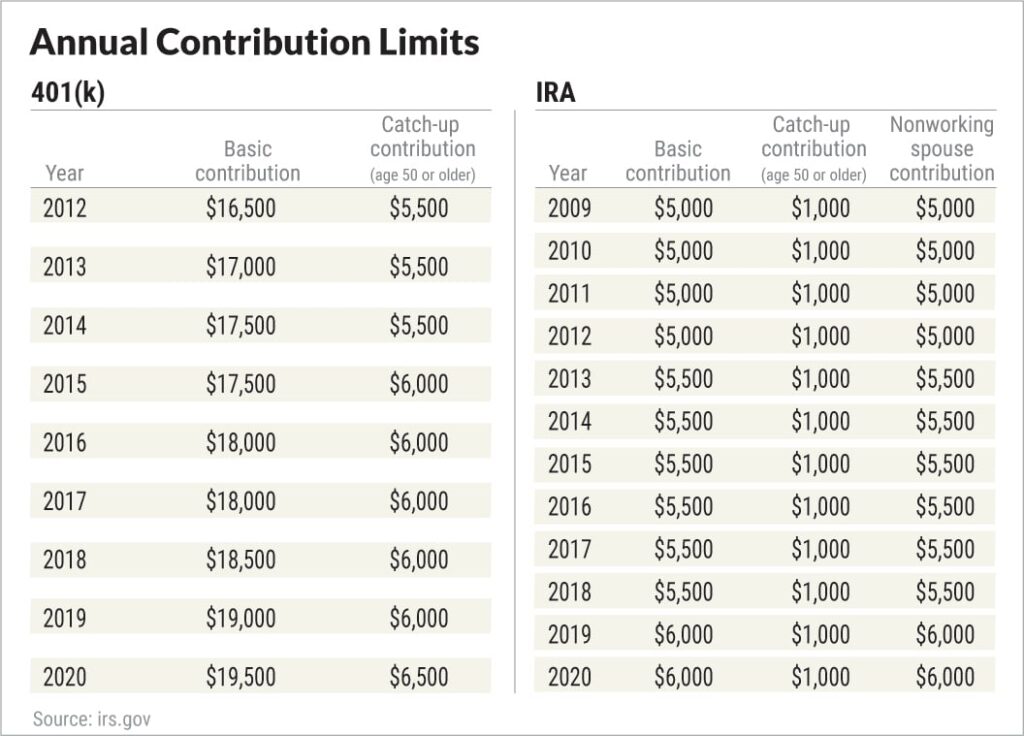

The annual contribution limit for IRAs is set by the IRS and can change each year. For 2024, the limit is $7,000, with an additional $1,000 catch-up contribution allowed for those age 50 and over. However, these limits are only part of the story. Income thresholds play a significant role in determining whether you can contribute to a Roth IRA and whether your traditional IRA contributions are tax-deductible.

For Roth IRAs, contributions are made with after-tax dollars, and earnings grow tax-free. However, if your modified adjusted gross income (MAGI) exceeds certain limits, your ability to contribute to a Roth IRA is phased out. For 2024, the Roth IRA contribution limit is phased out for single filers with MAGI between $146,000 and $161,000, and it’s completely eliminated for those with MAGI above $161,000. For those married filing jointly, the phase-out range is $230,000 to $240,000, with no contributions allowed above $240,000.

Traditional IRAs offer tax-deductible contributions, but this deduction may be limited if you (or your spouse) are covered by a retirement plan at work. If you are covered by a retirement plan at work, the deduction for traditional IRA contributions is phased out for single filers with AGI between $73,000 and $83,000 and is completely eliminated for those with AGI above $83,000. For those married filing jointly, the phase-out range is $116,000 to $136,000, with no deduction allowed above $136,000.

The key takeaway is that while an AGI of $2 million doesn’t directly prevent you from making a non-deductible contribution to a traditional IRA, it almost certainly eliminates your ability to contribute directly to a Roth IRA or deduct traditional IRA contributions if you are covered by a retirement plan at work.

The Impact of High AGI on Retirement Savings Options

When your AGI surpasses $2 million, your options for traditional retirement savings vehicles become limited. Direct contributions to Roth IRAs are off the table, and the tax deductibility of traditional IRA contributions is likely unavailable if you participate in an employer-sponsored retirement plan. This situation necessitates exploring alternative and more sophisticated strategies to maximize your retirement savings.

One of the most common strategies employed by high-income earners is the backdoor Roth IRA. This strategy involves making a non-deductible contribution to a traditional IRA and then converting it to a Roth IRA. Because you’re contributing after-tax dollars to the traditional IRA, the conversion to a Roth IRA is generally tax-free, assuming there are no pre-tax dollars in any of your traditional IRA accounts. This allows you to effectively bypass the income limitations associated with direct Roth IRA contributions.

Another option is to maximize contributions to employer-sponsored retirement plans, such as 401(k)s or 403(b)s. These plans often allow for pre-tax contributions, reducing your taxable income in the current year while simultaneously building your retirement nest egg. The contribution limits for these plans are typically higher than those for IRAs, providing a greater opportunity to save.

Beyond traditional retirement accounts, high-income earners may also consider exploring alternative investment options, such as real estate, private equity, or venture capital. These investments can offer potentially higher returns, but they also come with greater risk and complexity. It’s essential to consult with a qualified financial advisor before investing in these types of assets.

The Backdoor Roth IRA Strategy: A Detailed Guide

The backdoor Roth IRA is a popular and effective strategy for high-income earners to contribute to a Roth IRA despite exceeding the income limits. It involves two key steps: making a non-deductible contribution to a traditional IRA and then converting that contribution to a Roth IRA.

Step 1: Non-Deductible Contribution to a Traditional IRA

The first step is to make a non-deductible contribution to a traditional IRA. This means that you will not be able to deduct this contribution from your taxable income. The contribution limit for 2024 is $7,000 (or $8,000 if you’re age 50 or older). It’s crucial to ensure that this contribution is indeed non-deductible, as any deductible contributions will complicate the conversion process.

Step 2: Roth IRA Conversion

Once the non-deductible contribution has been made, the next step is to convert the traditional IRA to a Roth IRA. This involves transferring the funds from your traditional IRA to a Roth IRA. The conversion is generally a taxable event, but because you already paid taxes on the original contribution (since it was non-deductible), you will only owe taxes on any earnings or gains that have accrued in the traditional IRA. However, if you have any pre-tax funds in any traditional IRA accounts, the pro-rata rule will apply.

The Pro-Rata Rule: This rule states that when you convert a traditional IRA to a Roth IRA, the conversion is taxed based on the proportion of pre-tax and after-tax funds in all of your traditional IRA accounts. For example, if you have $90,000 in pre-tax traditional IRA assets and make a $10,000 non-deductible contribution, and then convert the $10,000, 90% of the conversion will be taxed, as 90% of your total traditional IRA assets are pre-tax. This can significantly reduce the tax advantages of the backdoor Roth IRA strategy. Therefore, it is crucial to consider your total traditional IRA assets before implementing this strategy.

Potential Pitfalls and Considerations

While the backdoor Roth IRA can be a valuable tool, it’s essential to be aware of potential pitfalls. The pro-rata rule, as mentioned above, can significantly reduce the tax benefits if you have substantial pre-tax funds in traditional IRAs. Additionally, it’s crucial to accurately track your non-deductible contributions to avoid being taxed twice on the same funds.

It’s also important to consider the timing of the conversion. Converting when the market is down can minimize the tax liability, as there will be fewer earnings to tax. Conversely, converting when the market is high can result in a larger tax bill.

Maximizing Employer-Sponsored Retirement Plans

For high-income earners, maximizing contributions to employer-sponsored retirement plans, such as 401(k)s, 403(b)s, and defined benefit plans, is a crucial strategy for building retirement savings. These plans offer several advantages, including pre-tax contributions, potential employer matching, and tax-deferred growth.

401(k) and 403(b) Plans

401(k) and 403(b) plans allow employees to contribute a portion of their salary on a pre-tax basis, reducing their taxable income in the current year. The contribution limits for these plans are significantly higher than those for IRAs. For 2024, the employee contribution limit is $23,000, with an additional $7,500 catch-up contribution allowed for those age 50 and over. Employer matching contributions can further boost your retirement savings. Some plans also offer a Roth 401(k) option, which allows for after-tax contributions with tax-free growth and withdrawals in retirement.

Defined Benefit Plans

Defined benefit plans, also known as pension plans, are less common than 401(k)s and 403(b)s, but they can be a valuable tool for high-income earners, particularly business owners. These plans provide a guaranteed level of retirement income based on factors such as salary and years of service. The contribution limits for defined benefit plans are generally higher than those for defined contribution plans like 401(k)s, allowing for more significant tax-deferred savings.

Considerations for High-Income Earners

When maximizing contributions to employer-sponsored retirement plans, high-income earners should consider the impact on their current cash flow and tax liability. While pre-tax contributions reduce taxable income in the current year, they also reduce the amount of money available for other investments or expenses. It’s essential to strike a balance between current financial needs and long-term retirement goals.

Additionally, high-income earners should be aware of the potential for required minimum distributions (RMDs) in retirement. RMDs are mandatory withdrawals from tax-deferred retirement accounts that must begin at a certain age. These withdrawals are taxed as ordinary income, so it’s essential to plan for the potential tax implications.

Alternative Investment Strategies for High-AGI Individuals

Beyond traditional retirement accounts, high-AGI individuals often explore alternative investment strategies to diversify their portfolios and potentially generate higher returns. These strategies can include real estate, private equity, hedge funds, and venture capital.

Real Estate

Real estate can be a valuable investment for high-AGI individuals, offering the potential for both income and appreciation. Rental properties can generate a steady stream of income, while the value of the property may increase over time. Real estate also offers tax advantages, such as depreciation deductions and the ability to defer capital gains taxes through a 1031 exchange.

Private Equity

Private equity involves investing in companies that are not publicly traded. These investments can offer the potential for high returns, but they also come with significant risk and illiquidity. Private equity investments are typically only available to accredited investors, who meet certain income or net worth requirements.

Hedge Funds

Hedge funds are investment partnerships that use a variety of strategies to generate returns. These strategies can include short selling, arbitrage, and leverage. Hedge funds are typically only available to accredited investors and charge high fees.

Venture Capital

Venture capital involves investing in early-stage companies with high growth potential. These investments are highly risky, but they also offer the potential for significant returns. Venture capital investments are typically only available to accredited investors.

Due Diligence and Risk Management

When considering alternative investment strategies, it’s crucial to conduct thorough due diligence and carefully manage risk. These investments can be complex and illiquid, so it’s essential to understand the potential risks and rewards before investing. Consulting with a qualified financial advisor is highly recommended.

Case Studies: Retirement Planning for High-Income Earners

To illustrate the concepts discussed in this article, let’s examine a couple of hypothetical case studies involving high-income earners and their retirement planning strategies.

Case Study 1: The Executive with a $2.5 Million AGI

Sarah is a senior executive at a tech company with an AGI of $2.5 million. She is covered by her company’s 401(k) plan, but her high income prevents her from contributing directly to a Roth IRA or deducting traditional IRA contributions. Sarah utilizes the backdoor Roth IRA strategy, making non-deductible contributions to a traditional IRA and then converting them to a Roth IRA each year. She also maximizes her contributions to her company’s 401(k) plan, taking advantage of both pre-tax and Roth options. Additionally, Sarah invests in real estate, purchasing rental properties to generate income and diversify her portfolio.

Case Study 2: The Entrepreneur with a $3 Million AGI

John is a successful entrepreneur with an AGI of $3 million. He owns his own business and has established a defined benefit plan to maximize his retirement savings. He also invests in private equity and venture capital, seeking higher returns to accelerate his wealth accumulation. John carefully manages his risk by diversifying his investments and consulting with a team of financial advisors and tax professionals.

Key Takeaways from the Case Studies

These case studies highlight the importance of utilizing a variety of strategies to maximize retirement savings for high-income earners. The backdoor Roth IRA, employer-sponsored retirement plans, and alternative investments can all play a role in building a secure retirement nest egg. It’s essential to tailor your approach to your individual circumstances and consult with qualified professionals to ensure that you’re making informed decisions.

Seeking Expert Advice and Professional Guidance

Navigating the complexities of retirement planning with a high AGI requires expertise and careful consideration of various factors. It’s highly recommended to seek advice from qualified financial advisors, tax professionals, and estate planning attorneys. These professionals can help you develop a customized retirement plan that aligns with your individual goals and circumstances.

A financial advisor can help you assess your current financial situation, develop a retirement savings plan, and select appropriate investments. A tax professional can help you minimize your tax liability and navigate the complex tax rules related to retirement accounts and investments. An estate planning attorney can help you create a comprehensive estate plan that ensures your assets are distributed according to your wishes.

When selecting professional advisors, it’s essential to choose individuals who are experienced, knowledgeable, and trustworthy. Look for professionals who have a proven track record of success and who are committed to acting in your best interests. Check their credentials, read reviews, and ask for references before making a decision.

Securing Your Financial Future

Planning for retirement with an AGI over $2 million presents unique challenges and opportunities. While traditional retirement savings options may be limited, strategies like the backdoor Roth IRA, maximizing employer-sponsored retirement plans, and exploring alternative investments can help you build a secure financial future. The key is to understand the rules, carefully manage risk, and seek expert advice. By taking a proactive and informed approach, you can optimize your retirement savings and enjoy a comfortable and fulfilling retirement.

If you are ready to take control of your financial future and explore how these strategies can be applied to your unique situation, contact a qualified financial advisor today. They can provide personalized guidance and help you navigate the complexities of high-income retirement planning.